These days, if you’re an entrepreneur, you’ve probably come across messages like these:

“International loan with no collateral”

“Foreign investor ready to inject immediate capital”

“Loan approval within one week”

When a business is growing or facing financial pressure, offers like these can seem extremely tempting — especially when traditional funding routes feel difficult, slow, or out of reach.

But here’s the harsh reality: a significant portion of these offers are not financial opportunities — they’re traps.

The model behind these scams is simple: they sell hope, create a sense of urgency, present a professional appearance… and ultimately, they take money from you before a single dollar ever reaches your account.

I recently followed one of these offers intentionally all the way to the final stages — not to receive a loan, but to carefully examine how they operate. What I discovered was so educational (and concerning) that I decided to share my experience.

A Real Experience + Critical Warning Signs

The purpose of this article is not to scare you.

The goal is to ensure that if you ever find yourself in a position where you truly need capital or financing, you make decisions based on awareness — not pressure, stress, or false hope. In the following sections, we’ll break down exactly how these fake offers work, the red flags they carry, and how you can identify them before it’s too late.

My Real Experience Testing a “Loan Offer”

To understand how these schemes actually work, I decided to go through the process myself — carefully and without sending any money.

It started with a very professional message. The tone was polite, the offer sounded structured, and the person claimed to represent an international funding group. They said they could provide both secured and unsecured loans — even though I clearly mentioned I had no collateral.

At first, they insisted they did not charge any registration or approval fees. That sounded reassuring — and that’s exactly how trust is slowly built.

But later, a document was sent with a different explanation. It said they required a “general expenses fee” from the borrower to cover loan-related costs such as processing and fund transfer.

In simple words: no fee for approval… but a fee before receiving the money.

That contradiction is where the reality becomes clear. The structure is designed to look legitimate while still leading to one outcome — the victim paying upfront.

Even more concerning, the document included threats stating that if payment was not made, the borrower could be reported to authorities such as:

- US State Department

- Immigration Services

- FBI

No legitimate private lender has the authority to report someone to government or federal agencies over a refused “processing fee.” This is a psychological pressure tactic used to intimidate victims into paying.

At this point, the pattern was obvious. The “loan” was never the real product. The upfront payment was.

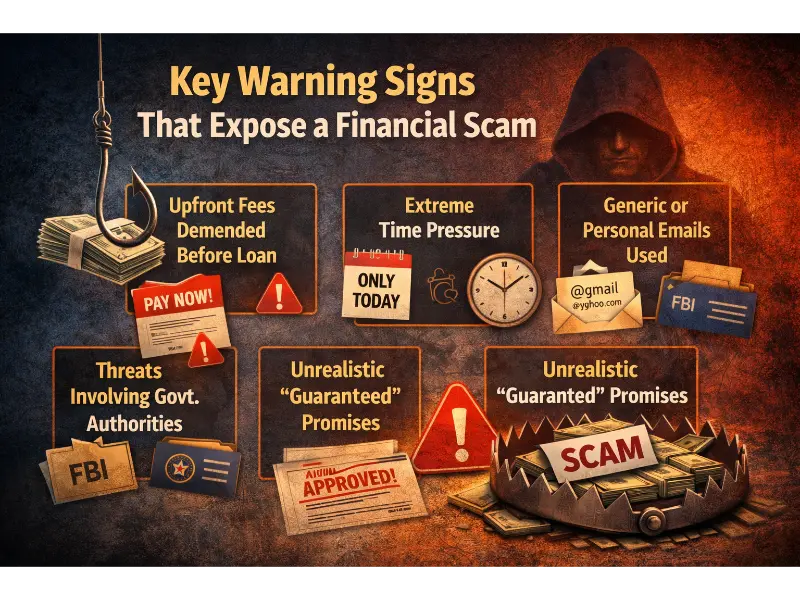

Key Warning Signs That Expose a Financial Scam

After observing this process up close, the scam pattern became very clear. Most of these offers begin with a professional appearance, but they share specific warning signs that—once you recognize them—allow you to spot the danger early.

1️⃣ Asking for Money Before Releasing the Loan

If someone tells you that before you receive any funds, you must first pay for things such as:

- Processing fees

- Loan insurance

- Transfer charges

- AML fees

- Capital release fees

- “General expenses fees”

You can say with near certainty that you are dealing with a scam.

Legitimate financial institutions, if they have fees at all, deduct them from the loan amount — they do not demand payment before any funds are disbursed.

2️⃣ Extreme Time Pressure

Statements like:

“This opportunity is only valid today”

“If you don’t pay now, your file will be closed”

“The investor is waiting for immediate confirmation”

These are all psychological pressure tactics. Scammers know that if you’re given time to think, you’ll likely notice inconsistencies.

Real investment opportunities do not pressure you to make rushed decisions without time for review, due diligence, or professional advice.

3️⃣ Using Generic Emails for Large Financial Deals

If the discussion involves hundreds of thousands or millions of dollars, yet communication happens through:

- Gmail

- Yahoo

- Personal Outlook accounts

- WhatsApp or Telegram with no verifiable corporate identity

You should be extremely cautious.

Legitimate companies handling serious financial negotiations use official domain emails and formal communication channels.

4️⃣ Threats Involving Government Authorities

If you see claims that failure to pay will result in you being reported to organizations such as:

- Ministry of Foreign Affairs

- Immigration authorities

- Federal police

- FBI

This is a major red flag.

No private financing company has the legal authority to make such reports. This is simply a fear tactic used to intimidate victims.

5️⃣ Unrealistic and “Guaranteed” Promises

Statements like:

“Guaranteed approval”

“No credit check”

“Zero risk”

“No collateral, no review, no limitations”

Do not exist in the real world of finance. Every legitimate investor and lender conducts a proper risk assessment before providing funds.

Looking Beyond Loans and Investors?

Sometimes the real growth accelerator isn’t more capital — it’s the right market partner.

A strategic partner can open distribution channels, bring customers, reduce risk, and scale your business faster than traditional financing alone.

Read: How the Right Market Partner Can Outperform Traditional Investments →

How to Professionally Evaluate an Investment or Loan Offer

Not every offer is a scam. Real investors and legitimate lenders do exist. The difference between a genuine opportunity and a trap lies in how you evaluate it.

In this guide, I’ll walk you through several practical steps that can save you from a costly mistake:

1️⃣ Verify the Real Identity of the Company or Individual

Don’t trust a polished website alone. Always check:

- Is there a company registration number, legal address, and verifiable information?

- Does the company or person appear in independent sources (not just their own website), and do they have a traceable history?

A simple search of the person’s or company’s name — even using AI tools — doesn’t take much time, but it can prevent a serious financial loss.

Real companies and real professionals leave real, verifiable footprints.

2️⃣ Check the Email Domain Carefully

An official investment or financial firm should normally communicate through a dedicated company domain email.

If negotiations involving large sums of money are happening through Gmail or other free email services, you should be extremely cautious.

Even if the other party uses a personal email, you can still look for supporting clues:

- Has this email address appeared on older online profiles?

- Was it used years ago on forums, websites, or social media?

- Has it shown up in old data breaches? (This may indicate age, not necessarily credibility.)

Tools such as:

- Have I Been Pwned

- Epieos

can show whether an email has existed in older databases. Being found in old breaches isn’t automatically bad — sometimes it simply shows the email has been active for many years.

If that email is linked to older accounts — such as long-standing YouTube channels, blogs, GitHub profiles, forums, or legacy social media accounts — you may find older activity dates that support the person’s digital history.

Brand-new email addresses with no historical footprint are a warning sign in large financial deals.

3️⃣ Consult a Legal or Financial Professional

Before signing any financial agreement — even if you urgently need the funds — get advice from a lawyer or an experienced financial professional.

Scammers rely on your urgency and stress to stop you from seeking proper advice.

4️⃣ Listen to Your Instincts

If something feels too good to be true, it probably is.

In legitimate financing processes:

✔ They ask many questions

✔ They request detailed documentation

✔ They take time for proper evaluation

They do not approve large funding quickly without serious review.

Final Thoughts

Financial scams usually begin with hope and end with loss, stress, and wasted time. But with a bit of awareness, patience, and careful verification, they can be avoided.

If you’ve had a similar experience, consider sharing it with others. Your experience might prevent someone else from becoming the next victim.

Frequently Asked Questions (FAQ)

1. How can I tell if an investment or loan offer is fake?

Fake offers usually include upfront fees, extreme urgency, guaranteed approvals, or communication only through personal emails and messaging apps. Legitimate funding processes involve due diligence, formal agreements, and verifiable company information.

2. Do real lenders ever ask for money before sending a loan?

Legitimate institutions may have fees, but they are typically deducted from the loan amount — not requested in advance through separate payments, especially not via crypto or personal accounts.

3. Is it safe to send my ID or passport to someone offering funding?

You should never share sensitive documents until you have verified the legal identity of the company and are working under formal agreements. Scammers often collect personal documents for identity misuse.

4. Why do scammers use pressure and urgency?

Urgency reduces critical thinking. When people feel rushed, they are less likely to verify details. Legitimate investors allow time for review and due diligence.

5. Are “guaranteed” approvals or “zero-risk” investments ever real?

No legitimate financial institution can guarantee approval without proper review. Promises of zero risk or guaranteed funding are major red flags.

6. How can I verify if a company or person is real?

Check for company registration records, legal addresses, independent mentions, and historical online presence. Real businesses leave a digital and legal footprint over time.

7. What should I do if I already paid a scammer?

Stop communication immediately, collect all evidence, and report the case to your bank, local cybercrime authorities, and the platform where the contact happened. Acting quickly increases the chance of mitigation.

The more informed you are, the harder it becomes for scammers to take advantage of you.

Need a second opinion on an investment or loan offer?

If you’ve received a funding offer and want a professional review before making any payment or commitment, I can help you assess its structure, credibility, and risk signals.